Building a strong credit portfolio takes time and consistent financial habits. The first step is to understand how credit reporting works and what factors lenders consider when evaluating your creditworthiness. From there, you can implement strategies that support healthy credit development. This article explains how to do that. Some key takeaways:

- While each lender may weigh factors differently, common elements used to assess creditworthiness include payment history, credit utilization, length of credit history, credit mix, and new credit inquiries

- Paying all your credit card and loan payments on time is one of the most important habits for maintaining a healthy credit profile. Keeping credit utilization maintained is another important habit.

- A diverse credit mix and a lengthy credit history are often viewed as signs of credit maturity, which can positively influence lending decisions.

Understanding these factors helps you make informed decisions about managing your credit accounts and building a portfolio that demonstrates financial responsibility.

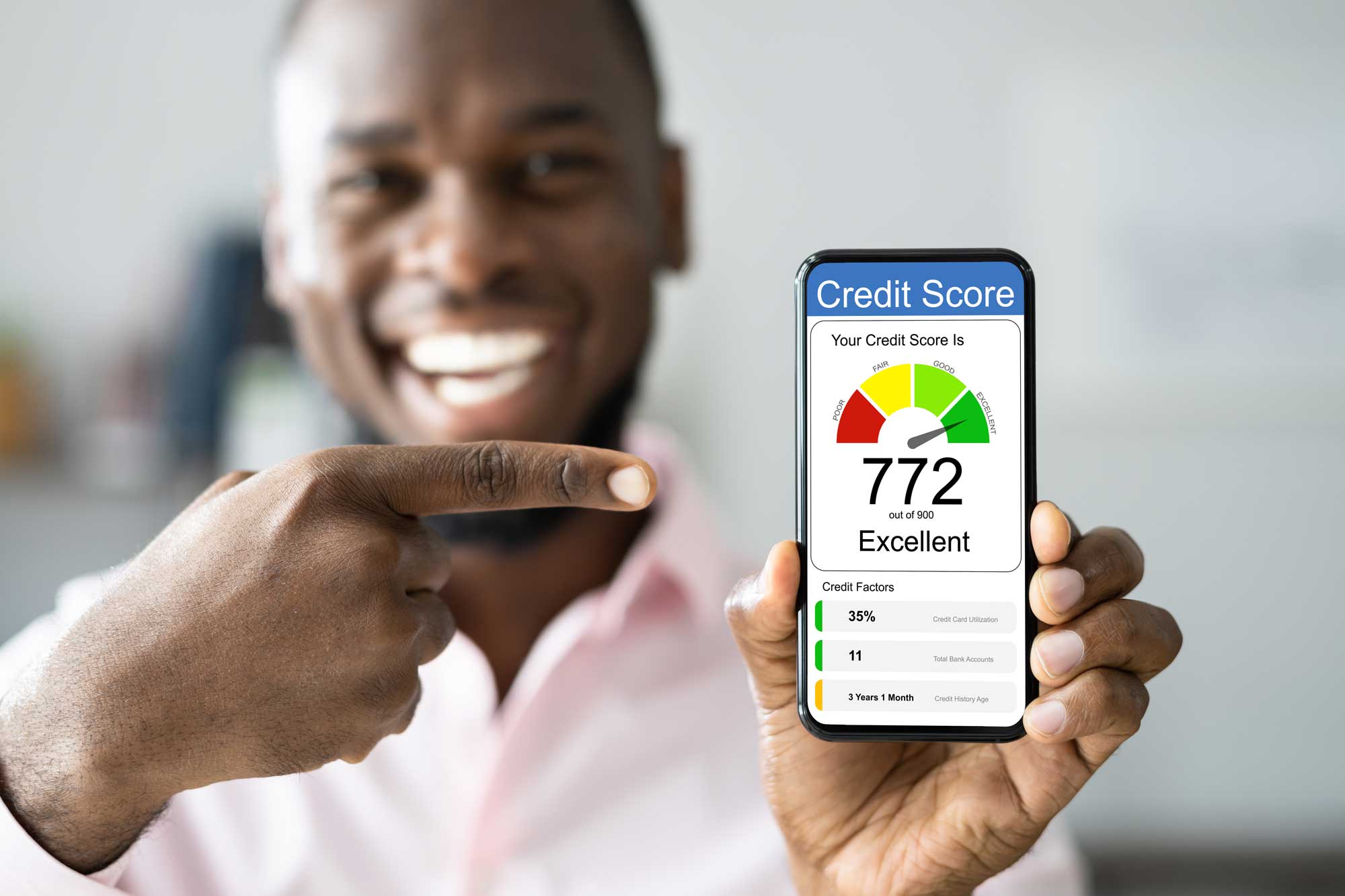

What Lenders Look At

There are five key factors that lenders typically evaluate when reviewing your credit profile. Learning about them is the first step in any credit-building process. We’ve listed all five below, along with their relative importance when lenders assess your creditworthiness:

- Payment History (Most Important): Payment history answers the most important question from lenders and credit card providers. Do you pay your bills on time? This factor makes it essential to prioritize timely payments. Late payments can negatively impact your credit standing.

- Credit Utilization (Very Important): Spending $4900 on a credit card with a $5,000 limit gives you a credit utilization rate of 98%. Banks and credit unions generally prefer to see that under 30% when you apply for a loan or line of credit. Mortgage lenders may ask you to pay off the full balance before they will allow you to mortgage a home.

- Length of Credit History (Important): Consumers with longer credit histories are considered “mature” candidates for loans and credit cards. Individuals with a short credit history may need a cosigner or collateral for a secured loan. Understanding this factor can help you make informed decisions about maintaining accounts over time.

- Credit Mix (Moderately Important): Credit mix is exactly what it sounds like. Lenders track what types of credit accounts you have. For example, an individual with an auto loan, an installment loan, credit cards, and a mortgage has a diverse credit mix. This demonstrates experience managing different types of financial obligations.

- New Credit Inquiries (Moderately Important): Applying for too many credit cards could increase the number of credit inquiries on your credit report. Ask if the lender is doing a “hard inquiry” or a “soft inquiry.” Hard inquiries are reported to credit bureaus.

8 Actionable Tips to Build Your Credit Portfolio

Tip #1: Make Payments on Time, Every Time

One way to help ensure your payments are made on time is to set them to autopay from your checking account. Payment history is the most important factor lenders consider, so it’s important to make timely payments, even if they’re only minimum payments. Missing payments can have a significant negative impact on your credit standing.

Tip #2: Keep Credit Utilization Low

Credit utilization shows lenders how responsibly you manage your credit. It can also influence whether lenders view you as able to handle additional credit accounts. Keeping balances well below your credit limits demonstrates responsible credit management.

Tip #3: Pay Down High Balances Strategically

Having several high credit balances at once can be overwhelming. Thankfully, you can start paying off your debt in small increments. Two proven strategies for this are debt avalanche, which focuses on paying high-interest-rate accounts first, and debt snowball, which advocates for paying off the smallest balances first. They’re both Dave Ramsey solutions.

Tip #4: Check Your Credit Report Regularly

Credit bureaus and credit reporting agencies occasionally make mistakes. It’s important to check your credit report regularly to ensure there are no errors that could affect how lenders view your credit profile. If you find any, request that the reporting agency investigate and correct them. Monitoring your report helps you stay informed about your credit standing. For a free copy of your credit report, visit FreeCreditReport.com.

Tip #5: Don’t Close Old Accounts

That store charge card that you applied for when you were a teenager is still valuable. It represents your first credit account. Consider keeping it open, even if you’re no longer using it regularly. Closing old accounts can affect the length of your credit history and your available credit, both of which are factors lenders consider.

Tip #6: Limit New Credit Applications

Each hard inquiry appears on your credit report, and multiple inquiries suggest you’re frequently seeking credit. While the impact of a single inquiry is usually modest, it’s worth being thoughtful about when and why you’re applying for new credit. Space out applications when possible and only apply for credit you genuinely need.

Tip #7: Diversify Your Credit Mix

Having different types of accounts can contribute to a well-rounded credit portfolio, especially if you have a limited credit history. Credit-builder loans and secured credit cards that report payments to the credit bureaus are options worth considering as you develop your credit history.

Tip #8: Become an Authorized User

Family members or good friends with strong credit can help you build your credit by allowing you to be an authorized user on their accounts. This obviously requires a high level of trust, but spouses and parents often do it for their respective family members. Companies will sometimes do it for employees. You might want to check with your job about that.

How Long Does Credit Building Take?

Building a strong credit portfolio is a gradual process, and timelines vary dramatically depending on your starting point and which strategies you implement. We’ve broken down a few scenarios by projected timeline below:

- Short-term actions (2-8 weeks): Some credit-related changes can happen within two months of specific one-time actions. Paying off a high balance is one of those. Correcting errors on your credit report by having inaccurate items removed is another. Check your report and your finances to see if you can take either of these actions.

- Medium-term progress (3-6 months): Once you’ve addressed any immediate issues, focus on the consistent actions that support healthy credit development over time. Establish a pattern of on-time payments. Be selective about the number of credit applications you submit. Become an authorized user for someone else if that option is available.

- Long-term development (1-7 years): Negative items like late or missed payments and bankruptcies eventually age off your credit report, but it takes time. Use that period to build a longer credit history, demonstrate sustained responsible credit management, and maintain balances at reasonable levels relative to your credit limits.

Common Myths About Credit

Misconceptions about credit can lead to poor decisions. Here are some persistent myths:

“Checking your credit affects your credit standing.”

False. Checking your own credit generates a soft inquiry that doesn’t impact how lenders view your credit. You should monitor your credit regularly.

“Carrying a balance helps your credit.”

False. You don’t need to pay interest to build credit. Paying off balances in full each month demonstrates responsible credit management by keeping utilization low.

“Closing accounts improves your credit.”

Usually false. Closing accounts typically affects your credit profile by reducing available credit and potentially lowering your average account age.

“All inquiries affect your credit equally.”

False. Soft inquiries (like checking your own credit) don’t impact your credit standing, while hard inquiries appear on your report when you apply for new credit.

“You need to use credit cards to build credit.”

Partially false. While credit cards are one of the most accessible ways to build credit, installment loans, mortgages, and other forms of credit also contribute to your credit portfolio.